a. 相當時間內,除非我們看到實體經濟重要侷限條件有改變,否則股市的最大影響因子應該還是貨幣因素。Fed之後收回貨幣的方法、速度與總量都很重要。

此結論還是繼續暗示:價值投資法在極端貨幣因素干擾下可以相當長時間失效。

b. 過去經濟學者普遍認為貨幣因素與真實世界存在的遲滯效應,恐怕因為科技便利、交易成本大幅下降、交易頻率大幅上升而遲滯時間越來越短。

參考文獻:

Milton Friedman, “A Natural Experiment in Money Policy Covering Three Episodes of Growth and Decline in the Economy and the Stock Market" Journal of Economic Perspective, Vol. 19, (Fall 2005)

Pierre-Olivier Gourinchas 與 Hélène Rey,二位經濟學家在2005年的論文"From World Banker To World Venture Capitalist: Us External Adjustment And The Exorbitant Privilege"研究發現,從1952~2004年美國持有外國資產的平均收益率是5.72%,外國持有美國資產的平均收益率則僅3.61%,相差2.11%。

這表示同樣$100投入,52年的時間後的差異是$1803.7 vs $632.25,二者是2.85倍。

經濟學家Michael D. Bordo & 加州柏克萊大學經濟系教授Barry Eichengreen 論文"A Retrospective on the Bretton Woods system" 研究指出:1945~1971年全球發生了38次金融危機,但布林頓森林協議被美國違約後的1973~1997年全球發生了139次金融危機。

i. 貨幣總量可以造成股市整體上漲,該文我引用了諾貝爾經濟學獎得主Milton Friedman的論文,同時點出該研究闡明貨幣總量的改變會進一步影響股市泡沫破裂後的走勢。

ii. 該文我也引用貨幣理論大師Allan Meltzer的研究,1941年到1945年這段時間Fed採取的貨幣寬鬆政策,造成股市年複合成長率高達51.5%,但同時段CPI年複合增長率僅5%左右。這意味股價與實體經濟不但可以脫鉤,而且幅度也可以相當巨大,時間可以相當長。而讀者應該注意的還有,從CPI去觀察通貨膨脹是無效且錯誤的角度。

iii. 該文我更直指:價值投資這個投資方法究其核心邏輯完全忽略了「貨幣因素」如此重要的侷限條件,而這是個大問題。也正因為如此,價值投資奉行者一旦碰上貨幣現象強烈變化時就容易手足無措、不知如何處置。這在2008年後的十年來最為明顯,就連巴菲特1965年以來的驚人長期績效也在近十年越趨平淡。

這是說,在當時我明白預言投資人將看到相當時期價值投資法失效的現象。

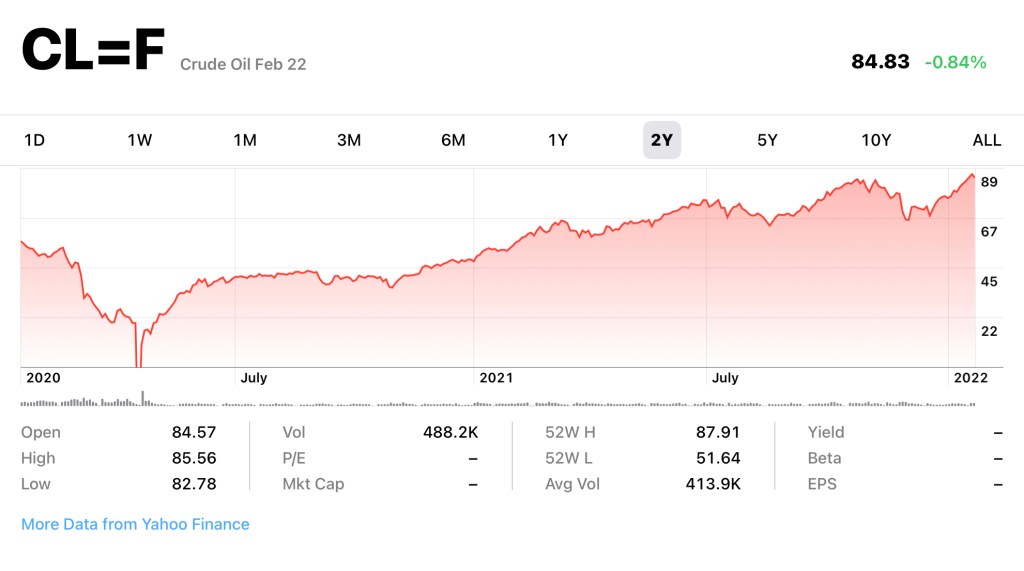

iv. 當時石油期貨的負價格(-$37.63USD/每桶)純粹是期貨契約操作下的極端特殊現象,事實上石油產業並沒有那麼糟,更不存在知名反指標台灣商業周刊宣稱的「石油紀元結束」。我也指出許多人油庫、游泳池甚至大型填充包儲存石油以待未來價格反彈的舉措。

這部分可以參閱Christopher J. Coyne 和Abigail R. Hall 這兩位經濟學家的新書「Manufacturing Militarism (製造軍國主義)」。書中從經濟學理論與歷史,爬梳美國從獨立戰爭、南北內戰、兩次世界大戰到最近的反恐相關戰爭,美國政客如何藉由操弄民意來創造戰爭。

例如我們都很清楚,事後諸葛證明伊拉克的海珊(Saddam Hussein )並未主導911恐怖襲擊也未有美國聲稱的大規模殺害武器。但兩位作者引用大量歷史資料證實當年小布希政府官員「所真實知悉的資訊與故意放給人民的消息存在巨大差異」 ,更透過「不知名官員透過聽話紐約時報記者放出『伊拉克有核武或類似生化武器』,被報導後再由時任國務卿Condoleeza Rice 與時任副總統 Dick Cheney 引用紐約時報,並稱是由獨立消息人士證實」的方式,創造美國國會與民意對伊拉克人人喊打的輿論環境。

「… 今年7月初美國總統Biden簽署了一系列行政命令,新增了橫跨農業、健康產業、物流、交通、科技產業、勞工…等各種管制,聲稱可以透過政府干預帶來產業競爭狀態的改善與消費者/勞工權益。 我們可以從Biden總統的發言看到他對基礎經濟學概念的嚴重無知與缺乏:“Capitalism without competition isn’t capitalism. It’s exploitation,” … “Without healthy competition, big players can change and charge whatever they want, and treat you however they want. And for too many Americans that means accepting a bad deal for things that you can’t go without.” 經濟學認為競爭無處不在,而不同的侷限條件會導致競爭的態樣改變。某些侷限條件下的競爭會有較高的租值消散,某些則較少。純粹市價競爭的自由市場是理論上完全無租值消散的一種競爭態樣。 因此,政府管制往往帶來的只是更多租值消散與尋租空間。誠如雷根總統說過:「政府本身就是問題,而不是解答。」 所以我們不難發現試圖以更多管制措施、更多政府干預來「使市場健康競爭」的Biden政府,必然是一場徒勞無功且弊病叢生的白工。只是所增加的交易費用,依然是由美國人民來承擔,這對通貨膨脹烏雲蓋頂的底層百姓而言,恐怕雪上加霜。…」

a. 在疫情(尤其是應付疫情的管制措施)影響與前述制度成本大幅上升的侷限下,我看不出未來十年美國實體經濟成長會有高度增長的可能,持平就很不錯了。除非出現如網際網路這種顛覆性科技普及的現象。

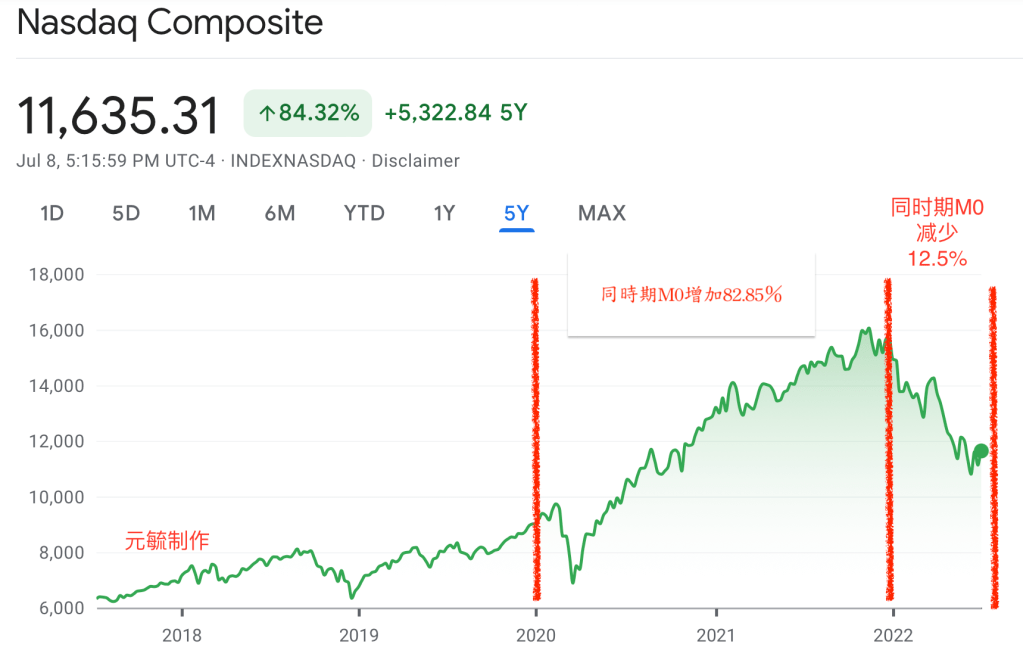

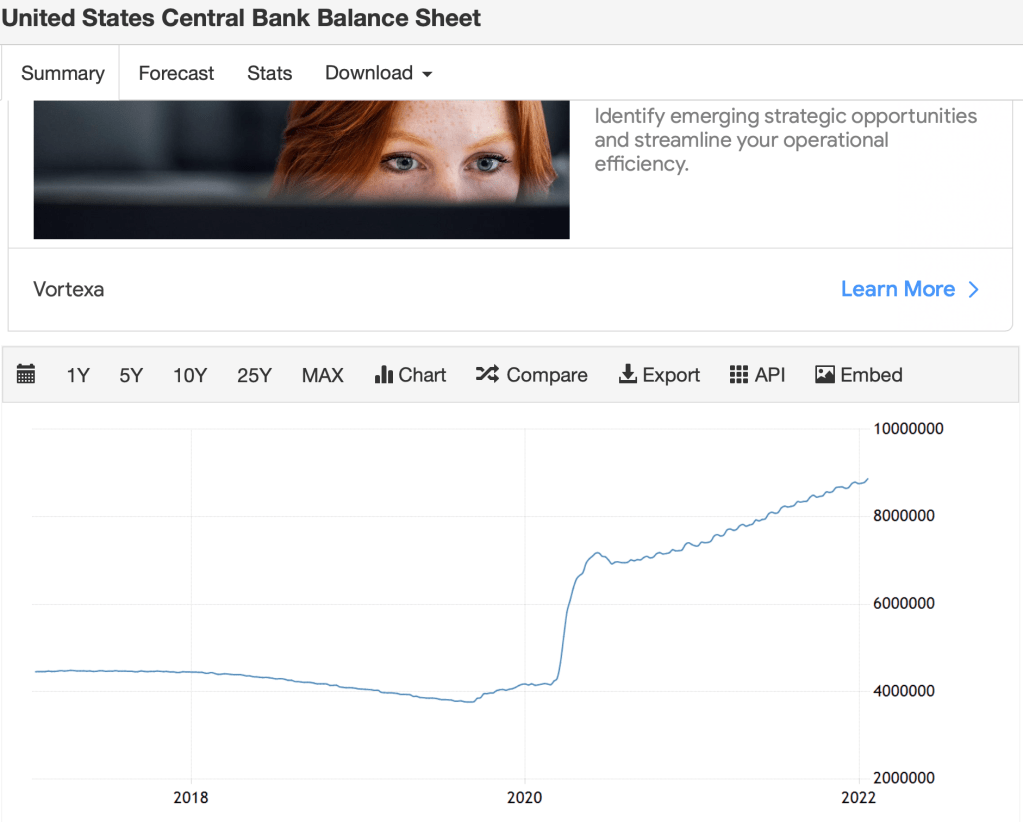

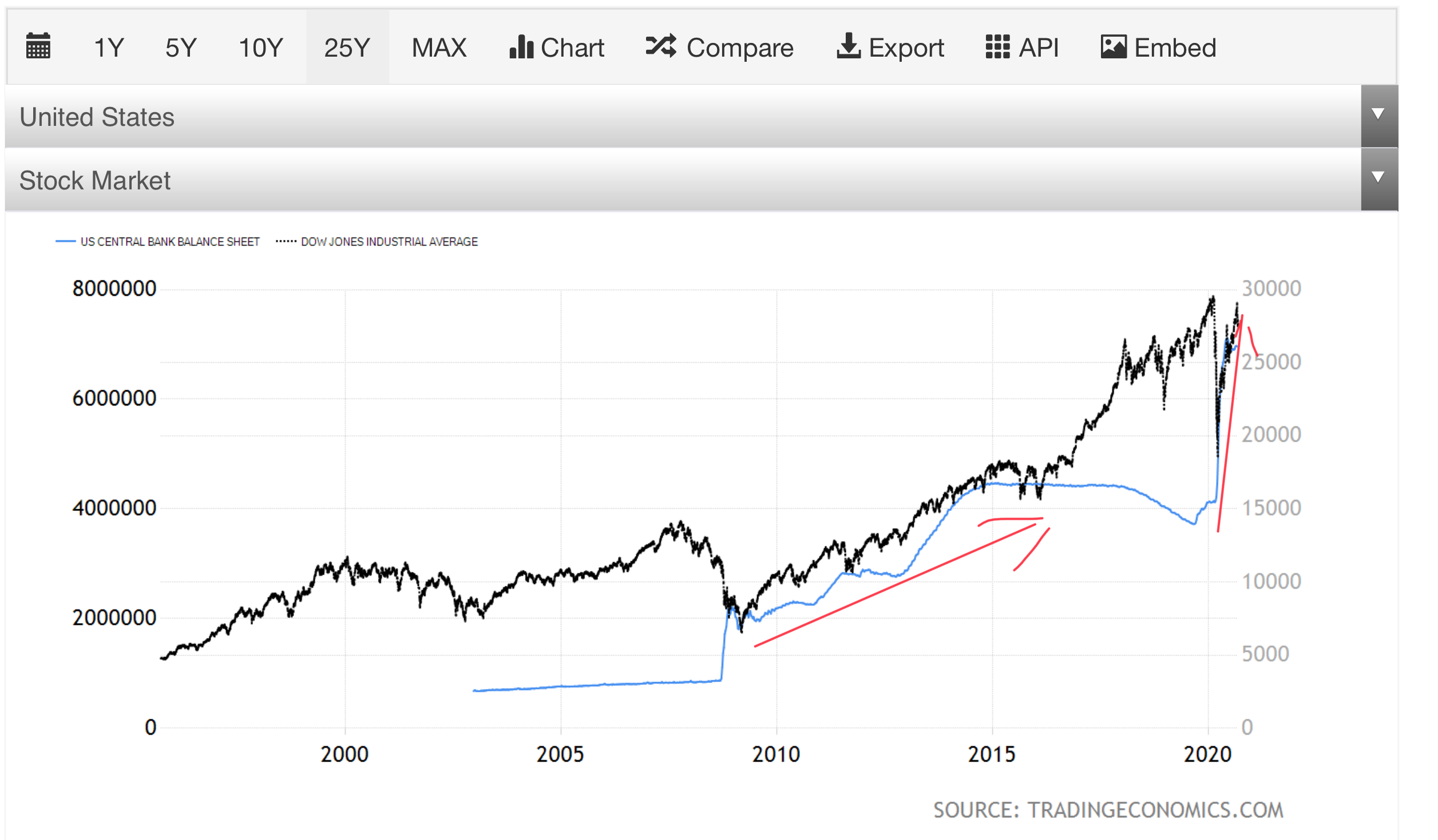

b. Fed在2020年初~2021年結束,短短兩年資產擴增2倍有餘,如此貨幣增長量是Fed設立以來未曾有的紀錄。換算年複合增長率超過41.4%,然而相對應的經濟增長卻完全脫鉤。

再強調一次,通貨膨脹來自於貨幣增長速度超過實體經濟成長速度。

故,相當長時間客觀環境都會在通貨膨脹與停滯型通膨之間徘徊。

這就來到本文第三部分…

三、停滯型通膨的客觀環境下該如何投資

2021年3月我在「近日股市資金行情之我見」(https://bit.ly/3qULiOG)文中即引用了經濟學大師Armen A. Alchian 1965年的論文 「Effects of Inflation Upon Stock Prices 」談通貨膨脹下股票標的如何選擇。

今天我再引用A. A. Alchian 和 R. A. Kessel合著的另一篇未曾發表的論文「More Evidence on Inflation-caused Wealth Redistribution」。

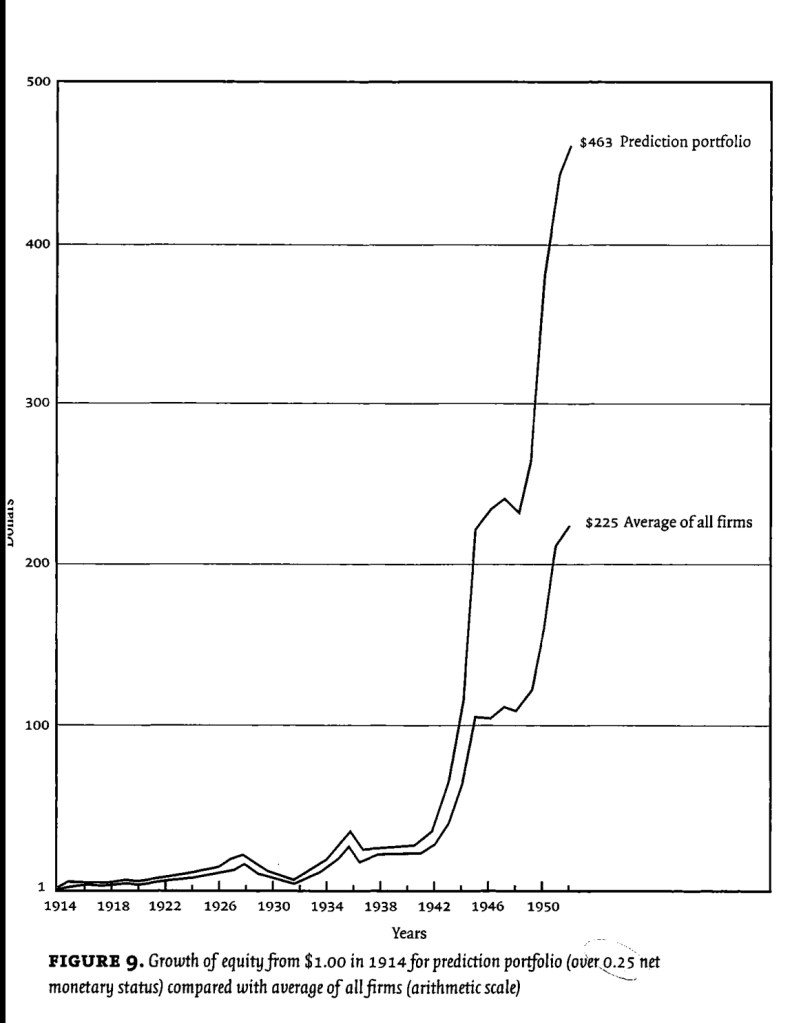

本文中兩位作者用20世紀上半葉美國股市的數據指出科學實證上的確存在一種利用通貨膨脹或緊縮來更快累積自身財富的方法,只要「資產配置者能:a. 正確預判通貨膨脹或緊縮,與b. 正確判斷投資標的公司的現金水位(To capture the wealth transfers, one would have to predict inflation or deflation, and he would also have to predict the net monetary status of any firm whose common stock he might hold in his portfolio. )」

我們從作者繪製的圖表可以看出,採取作者在"Effects"一文開發出之方法,36年的長期投資績效相差一倍有餘,換算年複合報酬率是18.59% vs. 16.24%。(見圖)

new March quarter records for both revenue and earnings, besting our year ago revenue performance by 54%.

iPhone, which grew 66% year- over-year driven by the strong popularity of the iPhone 12 family.

iPad grow very strong double digits to its highest March quarter revenue in nearly a decade.

In fact, the last three quarters for Mac have been its three best quarters ever

Wearables, Home and Accessories, which grew by 25% year-over-year.

Services. We achieved growth of 27% year-over-year and set new records for services in each of our geographic segments.

Over the next five years, we will invest $430 billion, creating 20,000 jobs in the process.

Luca Maestri

Our revenue reached a March quarter record of $89.6 billion, an increase of over $31 billion or 54% from a year ago.

Products revenue was a March quarter record of $72.7 billion, up 62% over a year ago.

Our services set an all-time record of $16.9 billion, growing 27% over a year ago. ( App Store, cloud services, music, video, advertising and payment services. Our new service offerings, Apple TV+, Apple Arcade, Apple News Fitness+)

Company gross margin was 42.5%, up 270 basis points from last quarter driven by cost savings, a strong mix and favorable foreign exchange. Products gross margin was 36.1%, growing 100 basis points sequentially also thanks to cost savings and FX, partially offset by seasonal loss of leverage. Services gross margin was 70.1%, up 170 basis points sequentially and mainly due to a different mix. Net income of $23.6 billion, diluted earnings per share of $1.40 and operating cash flow of $24 billion were all March quarter records by a wide margin.

During the March quarter, we added more than 40 million paid subs sequentially, and we have now reached more than 660 million paid subscriptions across the services on our platform. This is up $145 million from just a year ago and twice the number of paid subscriptions we are only 2.5 years ago.

Apple Watch continues to extend its reach, with nearly 75% of the customers purchasing Apple Watch during the quarter being new to the product.

Mac. We set an all-time revenue record of $9.1 billion, up 70% over last year, and grew very strongly in each geographic segment with all-time revenue records in Europe and rest of Asia Pacific and March quarter records in the Americas, Greater China and Japan. This amazing performance was driven by the very enthusiastic customer response to our new Macs powered by the M1 chip.

iPad performance was also outstanding with revenue of $7.8 billion up 79%.

And UCHealth, a large health care provider in Colorado, was able to reduce per patient vaccination time from 3 minutes to only 30 seconds largely by moving from PC stations to iPhones

We ended the quarter with over $204 billion in cash plus marketable securities. We issued $14 billion of new term debt and retired $3.5 billion of term debt leaving us with total debt of almost $122 billion. As a result, net cash was $83 billion at the end of the quarter.

we were also able to return nearly $23 billion to shareholders during the March quarter. This included $3.4 billion in dividends and equivalents and $19 billion through open market repurchases of 147 million Apple shares.

This will cause a steeper sequential decline than usual. Second, we believe supply constraints will have a revenue impact of $3 billion to $4 billion in the June quarter.

「Personal savings soared as high as 33.7% in April following the Cares Act and were still a healthy 13.7% in December before Congress passed another $900 billion in Covid aid. This means that, unlike during the 2009 recession, households aren’t weighed down by debt.

Personal bankruptcies, home foreclosures and loan delinquencies last fall were the lowest since at least 2003. The mortgage delinquency rate was 0.7% in the third quarter of 2020 compared to 7% in the first quarter of 2009. …」

高資產或高負債的公司在嚴重通膨時期的股價表現優於高現金部位的公司。在經濟學大師Armen A. Alchian 1965年的論文 “Effects of Inflation Upon Stock Prices “中,特別指出傳統經濟學如凱因斯、費雪等著名學者之見認為銀行身為典型債務人,在通貨膨脹環境下應該有較好的股價表現。而Alchian則點出這些學者大老忽略銀行雖然集債務於一身(大眾存款之於銀行就是債務),然而銀行受限於法規與現實,其資產多是「現金資產(money-type assets)」,故在嚴重通貨膨脹影響下,銀行實際經濟損失大過通膨泡沫所得,股價表現當然好不到哪去。

「…JPMorgan, said the size of the bitcoin market had grown to equal about a fifth of gold held for investment and trading purposes, with a market capitalisation for the cryptocurrency of $750bn at its peak earlier this year, meaning it “is far from a niche asset class”. 」

「…Analysts at Canadian insurance company Manulife said in late January that the expansion in central banks’ balance sheets and rising public debt would push investors further into alternative asset classes …」

「…Xangle showing that investors have lost more than $16bn to fraud since 2012 …」

b. 近日美國美國前25大銀行對私人之貸款佔總資產比例從去年54.1%下降之45.7%,且放在Fed reserve account總金額達$3.15兆美元。

(The 25 largest U.S. banks currently hold 45.7% of their assets in loans and leases, according to Fed data released Friday, down from 54.1% this time last year. .. reserve balances in their Federal Reserve depository accounts at sky-high levels, $3.15 trillion at present

)

通膨現象將會更嚴重,因為「…According to a recent House Budget Committee estimate, $1 trillion from last year’s bills hasn’t been spent—including $59 billion for schools, $239 billion for health care and $452 billion in small business loans. State and local governments added 67,000 jobs in January. They don’t need more federal cash. …」

根據德國Hertie School of Governance的教授Daniela Stockmann推估,雖然推特在中國被網路長城阻隔,但中國用戶卻從2016年的約1000萬人成長至2019年的3200萬人。 我相信稍微理解中國推特用戶之使用特點,都知道春色無邊滿場飛之外,順道圍觀川建國者大有人在。