作者一針見血地指出,諷刺的是,正是OpenAI與Anthropic的CEO們多年來高調警示自家產品的危險性、主動呼籲政府立法規管,才在客觀上為今日的監管困局埋下伏筆。《1950年國防生產法》(Defense Production Act of 1950)已被搬上枱面,一旦AI被列為國防關鍵產業,政府將取得凌駕一切的管控權。最壞的情景是:要麼投資者因管制過嚴而撤資,AI進步戛然而止;要麼前沿模型只能由政府出資並獨家使用,等同變相「充公」。

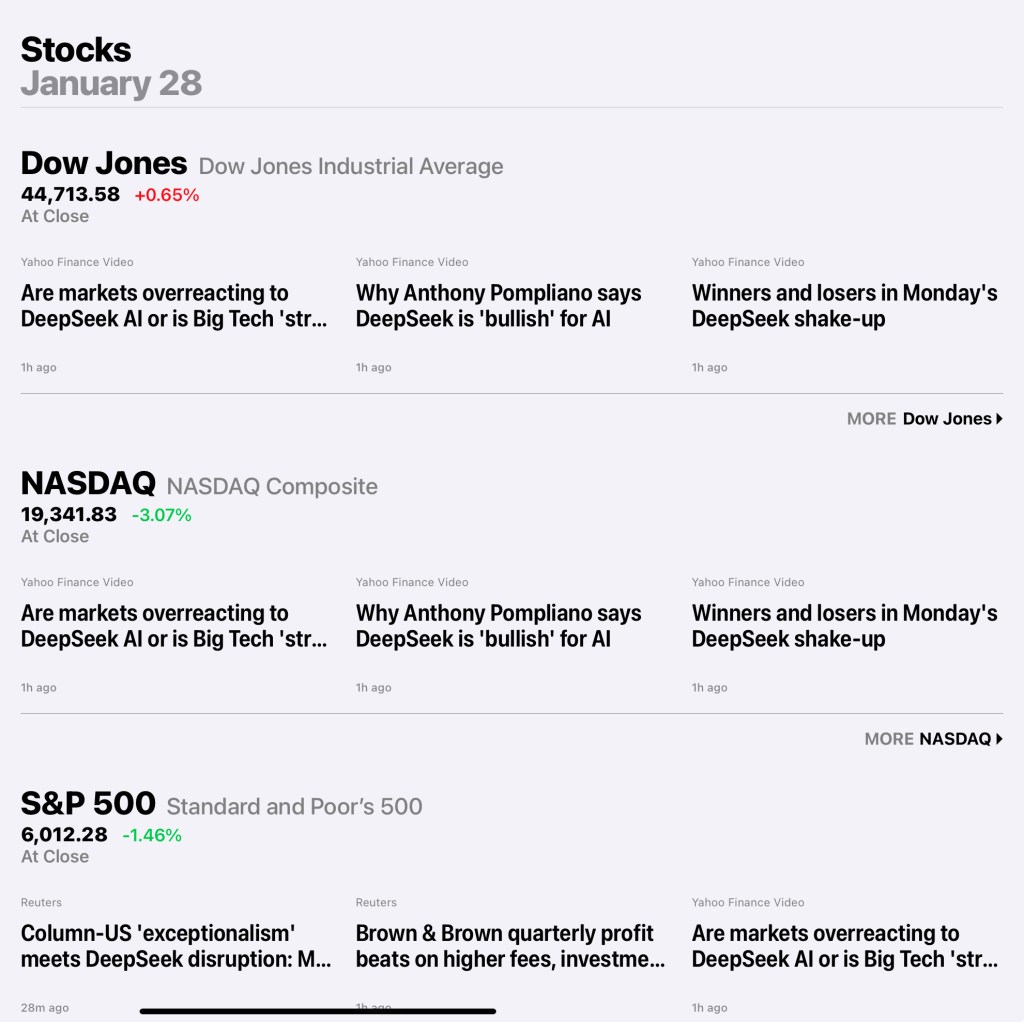

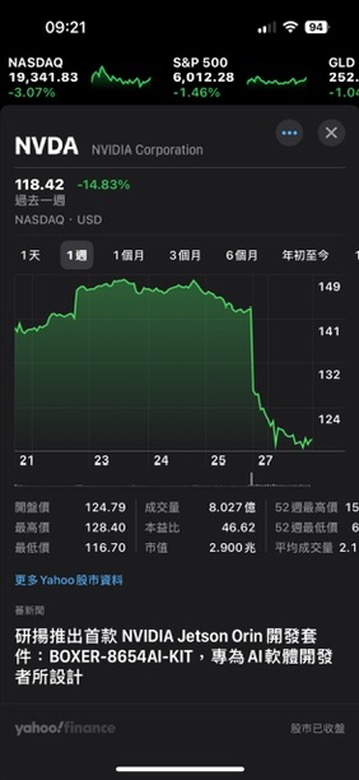

a. 用更便宜的鏟子也能挖金礦(也可以看成某工人用同樣的鏟子效率高過其他工人,經濟學上屬於一種專屬租值),對於降不了挖礦成本的其他礦工是否會構成競爭壓力?當然會。這是說,從經濟學競爭角度看,DeepSeek立即對OpenAI和Anthropic造成競爭和收入壓力是必然。如WSJ報導,使用DeepSeek的成本比Anthropic Claude降低至少75%!

new March quarter records for both revenue and earnings, besting our year ago revenue performance by 54%.

iPhone, which grew 66% year- over-year driven by the strong popularity of the iPhone 12 family.

iPad grow very strong double digits to its highest March quarter revenue in nearly a decade.

In fact, the last three quarters for Mac have been its three best quarters ever

Wearables, Home and Accessories, which grew by 25% year-over-year.

Services. We achieved growth of 27% year-over-year and set new records for services in each of our geographic segments.

Over the next five years, we will invest $430 billion, creating 20,000 jobs in the process.

Luca Maestri

Our revenue reached a March quarter record of $89.6 billion, an increase of over $31 billion or 54% from a year ago.

Products revenue was a March quarter record of $72.7 billion, up 62% over a year ago.

Our services set an all-time record of $16.9 billion, growing 27% over a year ago. ( App Store, cloud services, music, video, advertising and payment services. Our new service offerings, Apple TV+, Apple Arcade, Apple News Fitness+)

Company gross margin was 42.5%, up 270 basis points from last quarter driven by cost savings, a strong mix and favorable foreign exchange. Products gross margin was 36.1%, growing 100 basis points sequentially also thanks to cost savings and FX, partially offset by seasonal loss of leverage. Services gross margin was 70.1%, up 170 basis points sequentially and mainly due to a different mix. Net income of $23.6 billion, diluted earnings per share of $1.40 and operating cash flow of $24 billion were all March quarter records by a wide margin.

During the March quarter, we added more than 40 million paid subs sequentially, and we have now reached more than 660 million paid subscriptions across the services on our platform. This is up $145 million from just a year ago and twice the number of paid subscriptions we are only 2.5 years ago.

Apple Watch continues to extend its reach, with nearly 75% of the customers purchasing Apple Watch during the quarter being new to the product.

Mac. We set an all-time revenue record of $9.1 billion, up 70% over last year, and grew very strongly in each geographic segment with all-time revenue records in Europe and rest of Asia Pacific and March quarter records in the Americas, Greater China and Japan. This amazing performance was driven by the very enthusiastic customer response to our new Macs powered by the M1 chip.

iPad performance was also outstanding with revenue of $7.8 billion up 79%.

And UCHealth, a large health care provider in Colorado, was able to reduce per patient vaccination time from 3 minutes to only 30 seconds largely by moving from PC stations to iPhones

We ended the quarter with over $204 billion in cash plus marketable securities. We issued $14 billion of new term debt and retired $3.5 billion of term debt leaving us with total debt of almost $122 billion. As a result, net cash was $83 billion at the end of the quarter.

we were also able to return nearly $23 billion to shareholders during the March quarter. This included $3.4 billion in dividends and equivalents and $19 billion through open market repurchases of 147 million Apple shares.

This will cause a steeper sequential decline than usual. Second, we believe supply constraints will have a revenue impact of $3 billion to $4 billion in the June quarter.

Electric vehicle battery packs and motors currently cost about $4,000 more to manufacture than a comparable fossil fuel-burning midsize sedan engine. By 2022, the difference will be $1,900—and will disappear by mid-decade, according to investment bank UBS Group AG .

2010年1月時鋰離子成本約 $1,000 and $1,200 per kilowatt-hour. ,十年後為 $125 per kilowatt-hour

Intel still makes 80% of CPUs for personal computers and 94% of them for servers. Its estimated revenue of 2020 maybe about $75 billion USD, and its net income $20.7B.

Its major rivalry, AMD, has the estimated revenue of $9.47B, up from $6.73B a year earlier(40.7% growth, YoY) and estimated net income of $1.5B, up from $756M (98% growth,YoY).

It means that every dollar growth in revenue can bring 2.4 dollars growth in net income, which reflects the feature of high-rent-value business. The economic scale decides the gross profit margin.

And this is the reason why Intel enjoys higher marginal rent value than AMD.

Besides Intel’s dominant area, it had failed in RF and mobile device industry such as its doomed WiMax chipsets and mobile phone SoCs. Now it is facing two major problems: 1) its manufacturing skill has been left behind of TSMC for one or two generations; and 2) its lack of machine-learning products.

In the history, Intel had lost its competition against then Japanese companies in the RAM industry. Intel waived its white flag and turned into the CPU industry in 1980s. However, such successful turning point has never shown again since the launch of its wifi chipset. I do not have enough confidence in its new M&A strategy in the AI field.

On the other hand, the TSMC’s 2 nm manufacturing advance is not unreachable for Intel. I think the nature physical barriers, like the quantum tunnelling effect, will delay the progress of IC manufacturing after 2nm. Although I’ve heard and read many issues in its manufacturing team. I still believe Intel’s outstanding engineers can get things done after all. It only takes time and money. Nonetheless, this is another big problem. After TSMC having enjoyed monopoly profits for quite a long time, even Intel could catch up with TSMC after spending about couple years and billions dollars, the remaining rent value will be limited for Intel. I am not sure whether the necessary costs of competition would be covered or not, especially considering that Intel has lost its big client, Apple. Of course, the intense competition would erode TSMC’s rent value, too. It’s not a good news for TSMC’s investors who recently got on the board at such high stock prices.

University of St. Andrews的生物學教授Elena Miu與Luke Rendell研究Mathworks Software 舉辦的程式編碼競賽,從1998~2012年,共14年19場公開競賽,近2000位參賽者提供超過45000份原始碼。比賽雖是解決科學問題,但並不存在單一正確的解答。評審依據程式碼的簡潔性與可用性來評分。